Is the Oil Industry Dying?

August 10, 2016

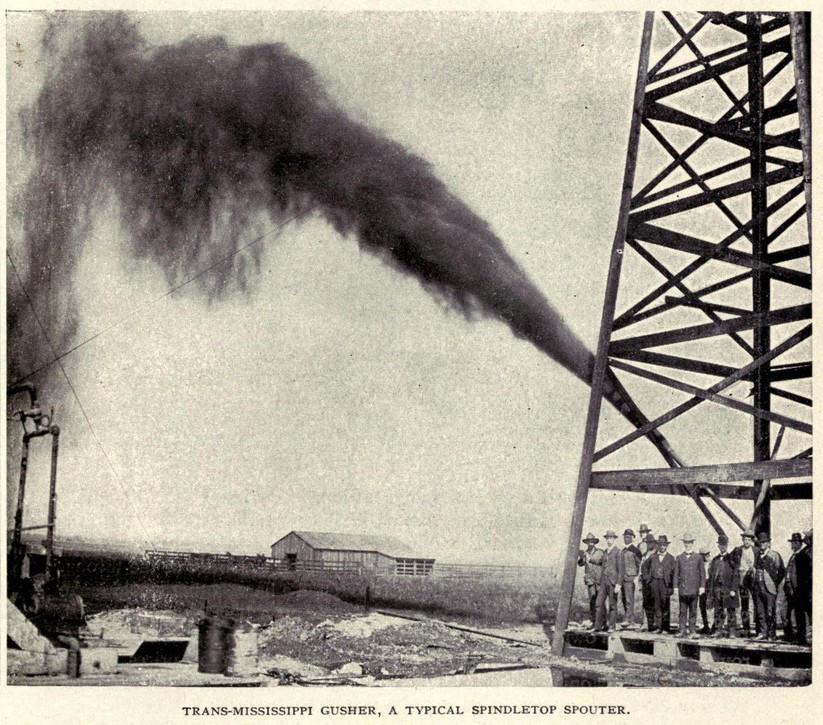

A spindletop spouter gushes oil in 1902. (Image: Wikimedia Commons)

Talking about “peak oil” can feel very last decade. In fact, the question is still current. Petroleum markets are so glutted and prices are so low that most industry commenters think any worry about future oil supplies is pointless. The glut and price dip, however, are hardly indications of a healthy industry; instead, they are symptoms of an increasing inability to match production cost, supply, and demand in a way that’s profitable for producers but affordable for society. Is this what peak oil looks like?

Back in the early years of the current millennium, I was among a handful of authors warning that world petroleum production rates would soon hit a maximum level and start to decline, and that the eventual result would be economic mayhem. But it’s now the latter half of 2016 and, according to the United States Energy Information Administration, world production of crude oil hit a new high in 2014 of almost 78 million barrels per day, while 2015’s average number was almost certainly higher still.

Yet something strange and ominous is indeed happening in the oil industry. And I’d argue that only those versed in peak-oil discourse are prepared to understand what that is, and what the likely emerging trends will be.

Aside from issuing forecasts regarding the timing of the inevitable moment when petroleum production would max out (yes, many of those forecasts proved premature), we peak-oil writers more importantly tended to agree on three key insights, all of them as valid now as ever:

- Oil is essential to the modern world. Energy is what enables us to do anything and everything, and oil is currently the world’s primary energy source. But oil’s role in society is even more crucial than that sentence might suggest. Nearly 95 percent of global transport is oil-powered, and if trucks, trains, and ships were to stop running, the global economy would grind to a halt almost instantly. Even electricity (which is the other main energy pillar of commerce and daily life) depends on oil: coal mining, transport, and processing depend on oil; much the same is true for natural gas, uranium, and the components of solar panels and wind turbines.

- Oil is hard to substitute. A colleague, the energy analyst David Fridley, and I recently finished a year-long inquiry into details of the necessary and inevitable transition from fossil fuels to renewable sources of energy. While lots of sunshine and wind are available, not all the ways we use energy will be easy to adapt to renewable electricity. Some of the biggest challenges we identified are in the transport sector. Electric cars are certainly feasible (more are on the road every year), but batteries alone can’t power heavy trucks, container ships, and large airplanes.There are other possibilities (including biofuels and hydrogen-based fuels made using electricity), but these are likely to be much more expensive and will require large energy inputs for their ongoing production. Moreover, transitioning to them will take major investment and infrastructure build-out occurring over two or more decades.

- Depletion of oil (and of other non-renewable resources) tends to follow the low-hanging fruit principle. Humanity has been extracting oil on an industrial scale for 150 years now. At first, all it took was identifying places where petroleum was seeping to the ground surface, then digging a shallow well. Today, globally, millions of old conventional oil wells lie depleted and abandoned. The primary remaining prospects for production include heavy oil (which requires expensive processing); bitumen (which must be mined or steam-extracted); tight oil (produced from low-permeability source rocks, which requires hydrofracturing and horizontal drilling, with typical wells showing a rapid decline in output); deepwater oil (which entails high drilling and infrastructure costs); or arctic oil (which has so far mostly proven cost-prohibitive). All of these options entail rapidly growing environmental costs and risks.

It’s that third point that helps explain the disturbing recent evolution of the petroleum world. Most industry analysts focus on oil prices, and it’s clear on this score that the market has gone seriously weird in recent years. In 2001, petroleum sold for about $20 a barrel, a price that sat well within a fairly narrow band of highs and lows that had bounded price for roughly 20 years following the politically generated oil shocks of the 1970s. But, by the summer of 2008, the price had ascended to the unprecedented, dizzying altitude of $147; then (following the cratering of the global economy) it plummeted to $37. Following that, prices gradually recovered to around $100, where they remained for nearly three years before sliding again, starting in mid-2014, to the high $20s, from which they have partially rebounded to today’s approximately $40…

READ FULL ARTICLE

Originally published at Pacific Standard.